Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Five numbers every buyer in Maryland, DC & Northern Virginia should know right now.

If you’ve been waiting on the sidelines for the “perfect” time to buy, here’s the honest truth: the perfect time rarely announces itself. But the numbers shaping today’s DMV market are clearer than the headlines suggest — and several of them quietly favor buyers. Here are five worth understanding before you decide.

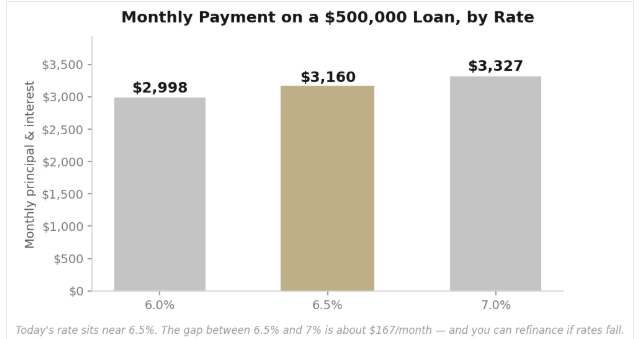

1. Rates have settled in the mid-6s — and you can “date the rate.”

The 30-year fixed is hovering around 6.5%, and economists expect it to stay above 6% through the rest of the year. That’s a different world than the sub-3% of a few years ago — but here’s what matters: you marry the house and date the rate. If rates drop later, you refinance. The home, the price you locked, and the equity you start building? Those are yours now.

2. Prices are steady — not crashing.

The median sold price across the DC metro is about $625,000, up roughly 1.3% from a year ago. Not a bubble, not a freefall — just steady. For anyone waiting for a big price drop, history and today’s tight supply suggest that bet is a risky one. Every month you rent is a month someone else builds equity on a home you could have owned.

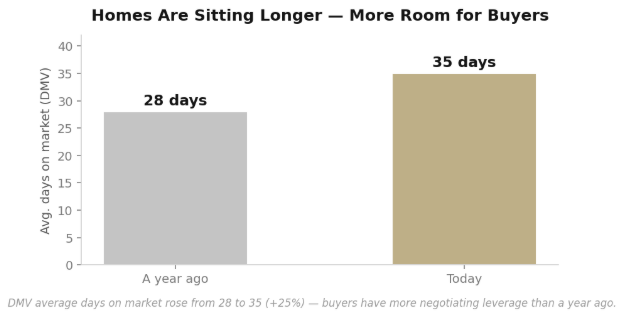

3. You have more room to negotiate than a year ago.

Homes are taking longer to sell — the DMV average rose from 28 days to 35 days on market. For buyers, slower means leverage: more time to think, more openings to negotiate price, closing-cost help, or repairs. The frenzied, waive-everything bidding wars have cooled.

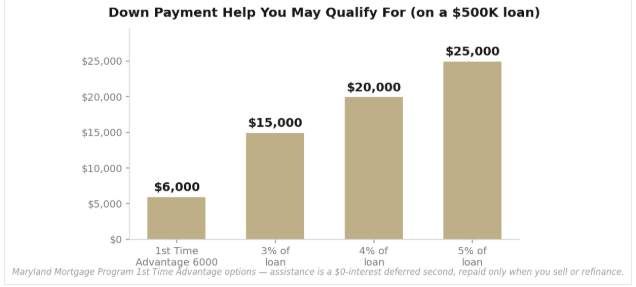

4. There’s down payment help most buyers never claim.

This is the big one. The Maryland Mortgage Program offers first-time (and many repeat) buyers down payment and closing-cost assistance — a flat $6,000 or 3–5% of your loan — as a $0-interest deferred second you only repay when you sell or refinance. In DC, DC Open Doors offers deferred down payment assistance with income limits high enough that buyers earning up to $275,400 can qualify. Many people who assume they can’t afford to buy simply haven’t been shown these.

5. The first step costs you nothing.

Before you fall in love with a listing, get a real pre-approval — it tells you your true budget, the programs you qualify for, and makes your offer competitive. It’s free, and it turns “someday” into a plan. Veterans: a VA loan can mean $0 down and no PMI, one of the strongest buying tools out there.